The Iranian rial: crash. The Turkish lira: crash. The Argentine peso: crash. The Brazilian real: crash. There are multiple, complex, parallel vectors at play in this wilderness of crashing currencies. Turkey’s case is heavily influenced by the bubble of easy credit created by European banks.

Argentina’s problem is mostly to do with the neoliberal austerity of President Mauricio Macri’s government admitting it won’t be able to fulfill payment targets agreed with the IMF less than three months ago.

Iran’s has to do with harsh United States sanctions imposed after the Trump administration’s unilateral pullout from the Iran nuclear deal.

This is a serious currency crisis affecting key emerging markets. Three of these – Brazil, Argentina and Turkey – are G20 members, and Iran, absent external pressure, would have everything to qualify as a member. Two – Iran and Turkey – are under US sanctions while the other two, at least for the moment, are firmly within Washington’s orbit.

Now, compare it with currencies that are gaining against the US dollar: the Ukrainian hryvnia, the Georgian lari and the Colombian peso. Not exactly G20 heavyweights – and all of them also inside Washington’s influence.

Behold the axis of gold

Independent analysts from Russia and Turkey to Brazil and Iran largely agree that the overwhelming factor in the current currency crisis is a reversing of the US Federal Reserve quantitative easing (QE) policy.

As investment banker and risk manager Jim Rickards noted, QE for all practical purposes represented the Fed declaring a currency war against the whole planet – printing US dollars at will on a trillion-dollar scale. That meant mounting US debt was devalued so foreign creditors were paid back with cheaper US dollars.

Now, the Fed has dramatically reversed course and is all-out invested in quantitative tightening (QT).

No more liquid dollars flooding emerging markets such as Turkey, Brazil, Argentina, Indonesia or India. US interest rates are up. The Fed stopped buying new bonds. The US Treasury is issuing new bond debt. Thus QT, combined with a global, targeted trade war against major emerging markets, spells out the new normal: the weaponization of the US dollar.

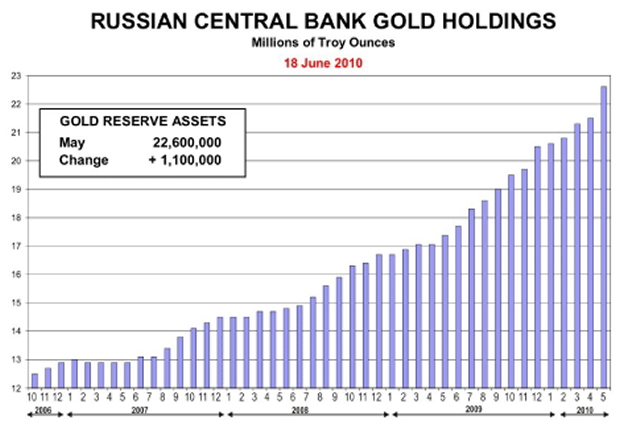

It’s no wonder that Russia, China, Turkey, Iran – nearly every major regional player invested in Eurasia integration – is buying gold with the aim of progressively getting out of US dollar hegemony. As JP Morgan himself coined it over a century ago, “Gold is money. All else is credit.”

Every currency war though is not about gold; it’s about the US dollar. Yet the US dollar now is like an inscrutable visitor from outer space, dependent on massive leverage; a galaxy of dodgy derivatives; the QE printing scheme; and gold not being awarded its true importance.

That is about to change. Russia and China are heavily invested in buying gold. Russia has dumped US Treasuries en masse. And what the BRICS had been discussing since the mid-2000s is now in motion; the drive to build alternative payment systems to the US dollar-subordinated SWIFT.

Germany appears to be coming around to the idea. If that does happen, it could possibly lead the way towards Europe redefining itself geopolitically in terms of its military and strategic independence.

When and if that happens, arguably at some point in the next decade, US foreign policy configured as an avalanche of sanctions may be effectively neutralized.

It will be a long, protracted affair – but some elements are already visible, as in China using US trading markets to help the emergence of a wider platform transference. After all key emerging markets cannot wiggle out of the US dollar system without full yuan convertibility.

And then there are nations contemplating the creation of their own cryptocurrencies. Digital finance is the way to go.

Some nations, for instance, could use a cryptocurrency denominated in SDRs (special drawing rights) – which is, in practice, the world money as designated by the IMF. They could back their new digital coins with gold.

Mired-in-crisis Venezuela is at least showing the way. The “sovereign bolivar” started circulating last week – pegged to a new cryptocurrency, the petro, which is worth 3,600 sovereign bolivars.

The new cryptocurrency is already posing a fascinating question: “Is the petro a forward sale of oil or an external debt backed by oil?” After all, BRICS members are buying a large chunk of the 100 million petros – confident that they are backed by a surefire reserve, the Ayacucho block of the Orinoco Oil Belt.

Venezuelan economist Tony Boza nailed it when he stressed the peg between the petro and international oil prices: “We are not going to be subject to the value of our currency being determined by a website, the oil market will determine it.”

A Persian cryptocurrency?

And that brings us to the key question of the US economic war on Iran. Persian Gulf traders are virtually unanimous: the global oil market is tightening, fast, and it will run short in the next two months.

Iran oil exports will likely drop to just over 2 million barrels a day in August. Compare it to a peak of 3.1 million barrels a day in April.

It looks like a lot of players are folding even before Trump’s oil sanctions kick in.

It also looks like the mood in Tehran is “we will survive,” but it’s not exactly clear the Iranian leadership is really aware of the nature of the incoming tempest.

The latest Oxford Economics report seems pretty realistic: “We expect the sanctions to tip the economy back into recession, with GDP now seen contracting by 3.7% in 2019, the worst economic performance in six years. For 2020, we see growth of 0.5%, driven by a modest recovery in private consumption and net exports.”

The authors of the report, Mohamed Bardastani and Maya Senussi, say “the other signatories to the original deal [the JCPOA, especially the EU-3] have yet to spell out a clear strategy that would allow them to circumvent US sanctions and continue importing Iranian oil.”

The report also admits the obvious: there will be no internal push in Iran for regime change (that’s a thing only happening in warped US neocon minds) while “both reformers and conservatives are united in defying the sanctions.”

But defying how? Tehran has not come up with a win-win roadmap capable of being sold to anyone – from JCPOA members to energy importers such as Japan, South Korea and Turkey. That would represent true Eurasia integration. Just having Ayatollah Khamenei saying Iran is ready to pull out of the JCPOA is not good enough.

What about a Persian cryptocurrency?

Pepe Escobar is correspondent-at-large at Asia Times. His latest book is 2030. Follow him on Facebook

The 21st Century