“All truth passes through three stages. First, it is ridiculed. Second, it is violently opposed. Third, it is accepted as being self-evident.” – Arthur Schopenhauer

The endless debate over when the Federal Reserve will raise rates is not only myopic, but misguided. It needs to stop, and more serious analysis must be done on the current state of financial markets and the transmission of monetary policy to the real economy. Looking at the S&P 500 (SPY), you would think we had one of the greatest economic and societal booms in history.

Yet, the only bull market trillions of dollars in stimulus has created is one in the wealth gap between rich and poor, as the “wealth effect” only ends up affecting the wealthy.

It needs to stop folks. The discussion should not be about when the Fed will raise rates, but why they haven’t been able to for so long and likely can’t in an aggressive way in the future.

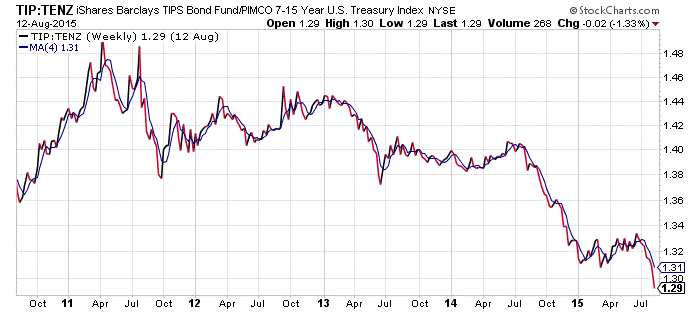

Take a look below at the price ratio of the iShares Barclays TIPS Bond Fund ETF (TIP) relative to the PIMCO 7-15 Year Treasury Index (TENZ).

As a reminder, a rising price ratio means the numerator/TIP (inflation protection buying) is outperforming (up more/down less) the denominator/TENZ (non-inflation protection buying).

The chart below essentially tracks market expectations. Notice that as everyone is endlessly talking about the Fed’s first rate hike, inflation expectations are utterly collapsing on the far right of the chart.

(click to enlarge)

Some will attribute this to oil, but inflation expectations have faltered really since the summer crash of 2011 took place despite a booming U.S. stock market. Stocks, by the way, are not meant to be a disinflation/deflation hedge, yet investors have piled into them so aggressively on the hopes that growth and inflation are about to ramp up.

They simply have not, and yield curve flattening remains a massive issue for central bank tightening. That behavior in the yield curve, confirmed by collapsing inflation expectations, tends to be an omen of bad things to come, as proven in the award winning paper I co-authored available by clicking here .

Something is ridiculously wrong here. It isn’t just the discussion over Fed policy. It’s the reality that all the money printing in the world isn’t translating into reflation. That is dangerous on many levels, and if the stock market begins to care about the fact that all of these tools central banks are using aren’t actually filtering to the economy, then the future is likely to be extraordinarily more volatile than the past.

For us, given the way we manage our investment strategies for our clients, we look forward to that because everything we do is focused on getting ahead of volatility before it hits.

For those looking at the stock market as proof of Federal Reserve power, the popping of the Last Great Bubble – faith in central banks – might make you challenge that belief soon enough.

This writing is for informational purposes only and does not constitute an offer to sell, a solicitation to buy, or a recommendation regarding any securities transaction, or as an offer to provide advisory or other services by Pension Partners, LLC in any jurisdiction in which such offer, solicitation, purchase or sale would be unlawful under the securities laws of such jurisdiction. The information contained in this writing should not be construed as financial or investment advice on any subject matter. Pension Partners, LLC expressly disclaims all liability in respect to actions taken based on any or all of the information on this writing.

See also Time For A Panic – Or A Picnic? on seekingalpha.com

Read more: http://www.nasdaq.com/article/something-is-still-ridiculously-wrong-cm508796#ixzz3jv08ZjAh